The UE rate is rising while comprehensive measures of US growth are steady and running above potential over the same period. That suggests that policy moves driven by heavily weighting UE rate shifts are likely to result in rates that are too dovish given conditions. Thread.

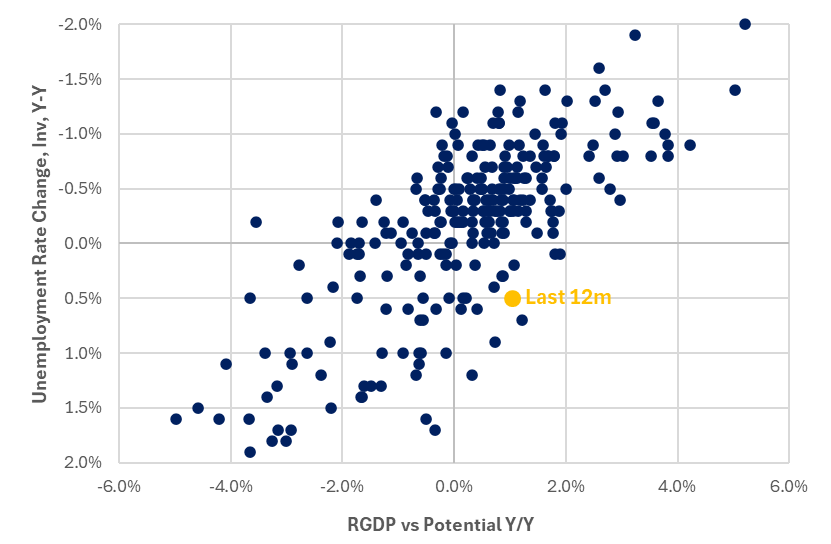

Conceptually unemployment should fall when the economy grows above its potential and rise in the opposite. Through time, this relationship has held quite strong - with a 90% correlation since 1950. With any perspective, the last 12m have been quite an outlier.

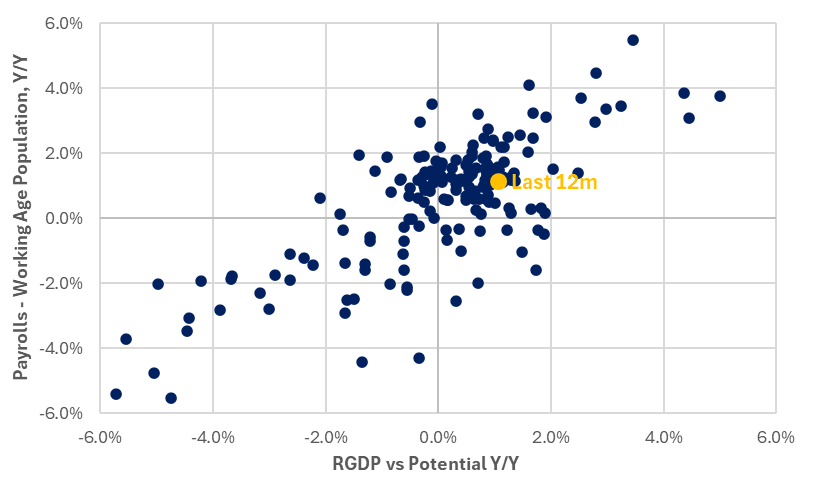

The payrolls numbers do not show a similar outlier relative to the real growth of the economy over the same time frame. Payroll growth relative to working ago population growth has been roughly in line with Real GDP growth relative to potential.

Further, the UE rate trend has diverged considerably over the last year from more comprehensive measures of growth which have been pretty steady over the last year (and up from the year prior).

While payroll growth has moderated from the strength seen just after the post-covid opening, the figures over the last year or so have remained relatively steady in comparison to working age population growth.

Further a broader look at similar data at least through last month suggests relatively stable employment conditions had been pretty stable for the last year or so (challenger, adp, IC, CC, etc). Nothing consistent with a sharp UE rate rise.

The labor market remains secularly tight, is still growing, but slowing relative to the last couple years, all while wage growth remains elevated.

— Bob Elliott (@BobEUnlimited) July 5, 2024

Ahead of today's report, a scan through the data reported so far this month for a sense of what's likely to come. Thread.

So while comprehensive measures of GDP, payrolls, and other employment measures have remained pretty steady over the last year, the UE rate stands in contrast - moving sharply higher over the last year or so.

This picture suggests that the sharp rise in the UE rate is more likely the outlier amongst the overall macro growth data, rather than most reflective of a well-triangulated set of data across the economy.

This shouldn't be a surprise since by its nature the household survey, which has a confidence interval that is roughly 4x the size of payrolls. And that variance is likely even wider given low response rates.

In such a situation, the prudent thing to do is look more comprehensively at the range of data available rather than focus on one measure given the possible uncertainty in what it is conveying.

From a policy makers perspective, this suggests that a heavy focus on the UE rate (and its derivations like JOLTS) may paint a picture of the labor market that is weaker than the actual reality.

With nearly 175bps of cuts px in over the next year and term premiums on long-bonds falling, markets are taking the UE rate shifts as the truth. A more comprehensive view suggests caution since the UE rate may be more of an outlier than the reality of the underlying dynamics.